World Bank East Asia and the Pacific Economic Update, April 2023: Reviving Growth

订阅

Download → Full Report

Summary

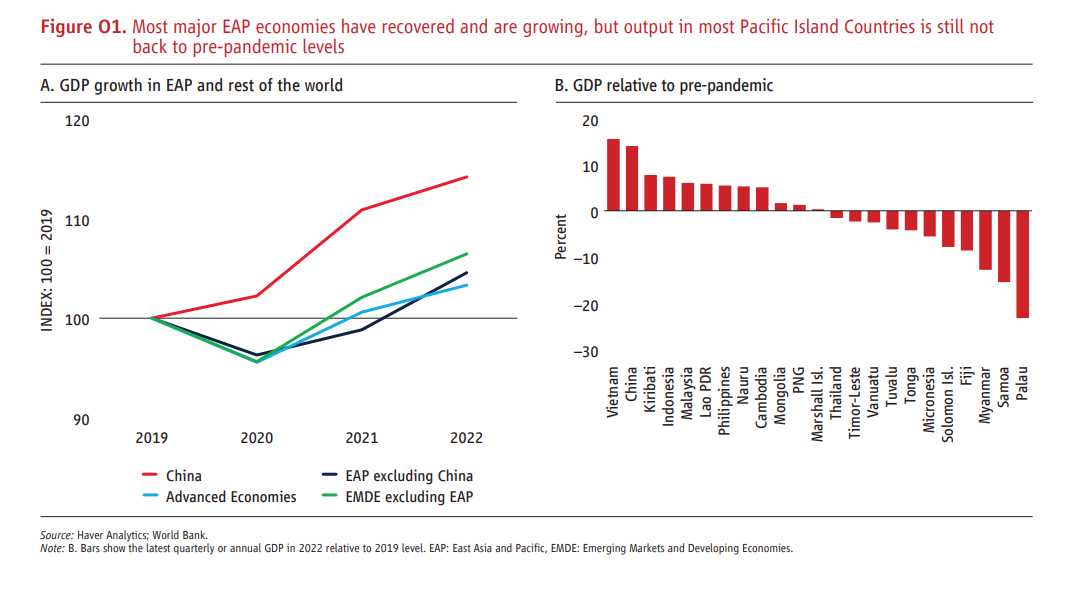

Economic activity in most of developing East Asia and Pacific (EAP) has recovered from the recent shocks, with goods exports and private consumption leading the way. However, output remains below pre-pandemic levels in many of the Pacific Island Countries. Inflation remains higher than target ranges in some countries. Near-term growth will depend on: global growth, projected to be slower in 2023 than in 2022, though recent projections are more optimistic; commodity prices, which have moderated; and financial tightening, which is likely to continue in the face of inflationary pressures in the US.

Taking a longer view of the more than two decades since the Asian Financial Crisis (AFC), growth in the developing economies of East Asia and the Pacific has been faster and more stable than in much of the rest of the world. The result has been a striking decline in poverty and, in the last decade, also a decline in inequality. During both the Great Recession and the COVID pandemic, the economies of the region proved more resilient than most.

But it would be a mistake to let these achievements obscure vulnerabilities, past, present, and future. Looking back, sound macroeconomic management after the AFC was accompanied only to a limited extent by productivity-boosting structural reforms. The convergence of the EAP countries with high-income countries, which was previously faster than in other emerging market and developing economies, has recently stalled. Now, the damage done by the pandemic, war, and financial tightening to people, firms, and governments, threatens to reduce growth and increase inequality. The region must cope with these problems even as it faces up to the major challenges of de-globalization, aging and climate change, to which it is particularly susceptible because it has thrived through trade, is growing old fast, and is both a victim of and contributor to climate change.

Four types of policy action are necessary.

• Macro-financial reforms to support recovery today and inclusive growth tomorrow.

• Structural reforms to boost innovation and productivity across the economy.

• Climate-related reforms to enhance resilience through efficient adaptation.

• International cooperation on climate mitigation, and to ensure openness to trade, investment, and technology flows, ideally multilaterally, but also regionally and bilaterally.

Overview

Recent developments

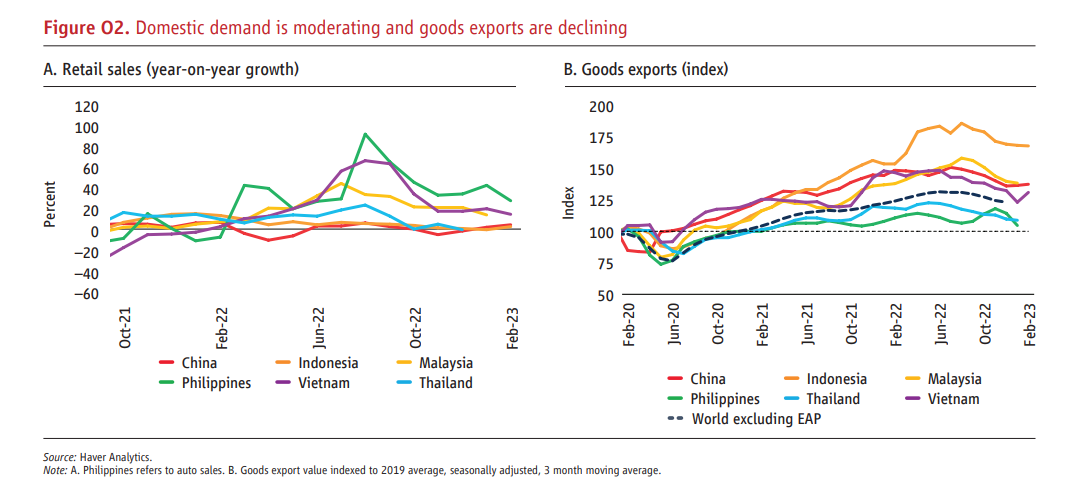

Growth in the region has been driven primarily by strong private consumption and goods exports. But now there are

signs of weakening domestic and foreign demand (figure O2).

Growth in the region has been driven primarily by strong private consumption and goods exports. But now there are

signs of weakening domestic and foreign demand (figure O2).

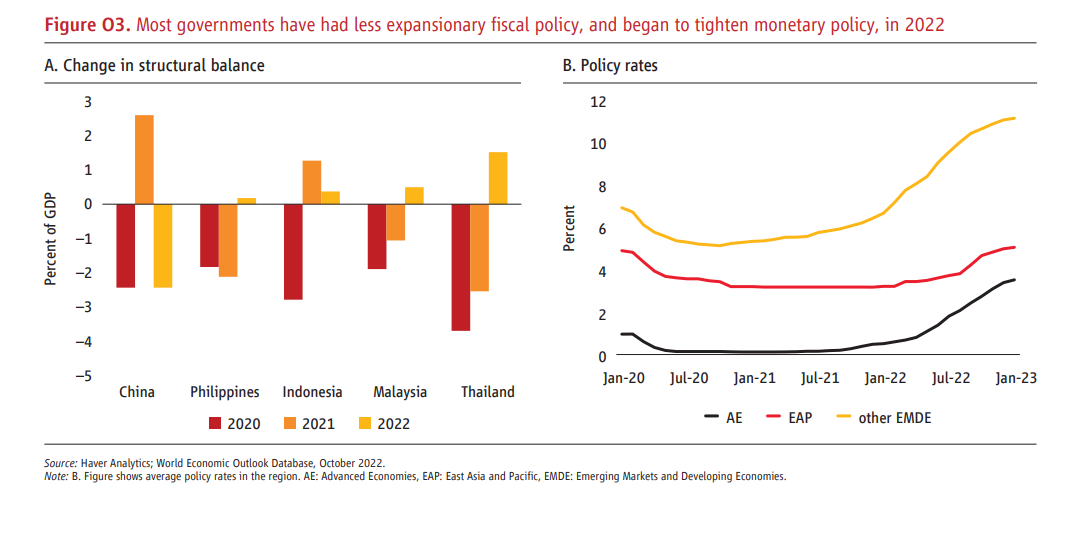

At the same time, macroeconomic policy was becoming less expansionary in most EAP countries. While China provided significant fiscal stimulus in 2022, fiscal support in other countries was diminishing. Even though interest rates were lower in EAP than in other emerging markets and developing economies (EMDEs), they have recently been increasing (figure O3).

Read The Whole Passage

First, please LoginComment After ~